Apr 17 2026 00:00

Before the Next Hurricane: What Your Insurance Must Cover

Living in New York or Florida means hurricane season isn’t just a possibility it’s a reality. Whether it’s a direct hit or a powerful outer band of wind and rain, storms can cause tens of thousands of dollars in damage within minutes. Before the next hurricane arrives, it’s critical to make sure your insurance policy actually protects you the way you think it does.

Here’s what every homeowner should double check long before the winds start picking up.

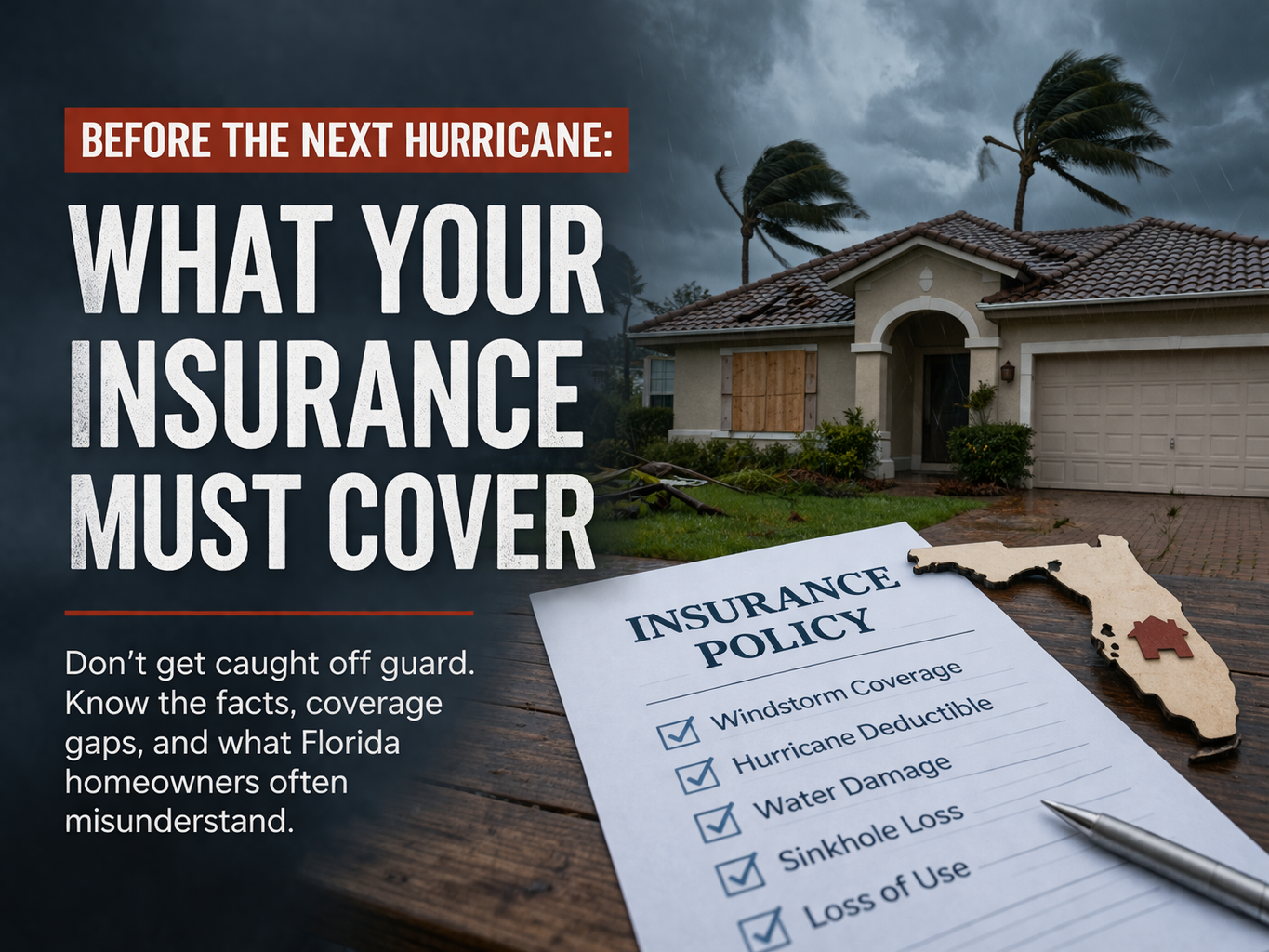

1. Windstorm & Hurricane Coverage

Most homeowners policies in hurricane‑prone regions include windstorm coverage but the details vary by carrier and state.

Key thing to check:

Do you have a separate hurricane deductible? In both Florida and some parts of New York, hurricane deductibles are usually a percentage of your dwelling coverage (2%–10%), not a flat dollar amount.

Example:

For a $400,000 home, a 5% hurricane deductible = $20,000 out of pocket

before insurance pays.

2. Flood Insurance (Not Included in Your Homeowners Policy)

Hurricanes bring storm surge and heavy rainfall and standard homeowners insurance does NOT cover flood damage.

Flood insurance must be purchased separately through the National Flood Insurance Program (NFIP) or private flood carriers.

Even if you’re not in a flood zone, flood coverage is strongly recommended.

3. Water Backup & Sewage Coverage

Storms can overload drainage systems and cause sewage or water backup inside your home.

Most homeowners policies exclude this unless you add an endorsement.

Check your policy for:

- Water/sewer backup coverage

- Sump pump failure coverage

- Interior drainage protection

This add‑on is affordable and worth every penny during hurricane season.

4. Roof Coverage & Roof Age Restrictions

Many Florida and coastal New York insurers have strict rules about roof age and condition.

Your policy may limit or deny coverage if:

- Your roof is older than the carrier’s guidelines

- You have missing shingles or existing damage

- Your roof type isn’t approved for hurricane zones

Review your roof’s age and make repairs before hurricane season begins.

5. Ordinance & Law Coverage (Building Code Upgrades)

After a hurricane, homes must be rebuilt to current building codes which are stricter than they were years ago.

Your standard policy may NOT fully cover the cost of required upgrades.

Ordinance & Law coverage pays for:

- Demolition

- Debris removal

- Rebuilding to current code

Without this endorsement, you may face thousands in uncovered costs.

6. Personal Property Replacement Cost

After a hurricane, replacing damaged belongings can be expensive. Make sure your policy covers replacement cost, not actual cash value (ACV).

Replacement cost= brand‑new items

ACV= depreciated value

This difference can be thousands of dollars.

7. Additional Living Expenses (ALE)

If your home becomes unlivable, ALE pays for:

- Temporary housing

- Food costs

- Laundry and additional living expenses

Check your limit it may not be enough for high‑cost areas or extended rebuilds.

8. Car Insurance for Hurricane Damage

Your auto insurance plays a role too. Only comprehensive coverage protects your vehicle from:

- Flooding

- Fallen trees

- Wind damage

- Flying debris

If you don’t have comprehensive coverage, your car likely isn’t protected.

Hurricane Season Isn’t the Time to Guess Get Protected Now

Insurance is one of the most important tools you have to protect your home and family during hurricane season. A quick review can help identify gaps, avoid costly surprises, and ensure you’re fully prepared before the next storm hits.

Call The Michaels Group for a Free Quote or Coverage Review

Florida:

386‑274‑8150

New York:(631) 629‑2233

We’ll compare options across 25+ carriers and help you choose the right protection before the next hurricane heads your way.